Skip to content

Skip to content

What prosperity looks like through disciplined budgeting

Prosperity goes beyond bills paid on time. It means having clear control over your money and steady, dependable growth. A simple budget reveals where every dollar goes and empowers you to progress toward meaningful goals with confidence.

A well crafted budget ensures essentials, like housing and utilities, are covered while you set aside funds for savings and the things you value. That balance creates steadiness and hope, not stress.

How budget rules shape long term wealth

Rules provide a clear map for your money. They show where to allocate each paycheck and how to protect your financial future. Following budget rules helps you:

- Create a budget that fits your life

- Build an emergency fund for unexpected events

- Move money into savings and retirement over time

Smart rules also simplify money management so you can spend on essentials while steadily pursuing long term goals. Start with small, consistent steps and watch your wealth grow.

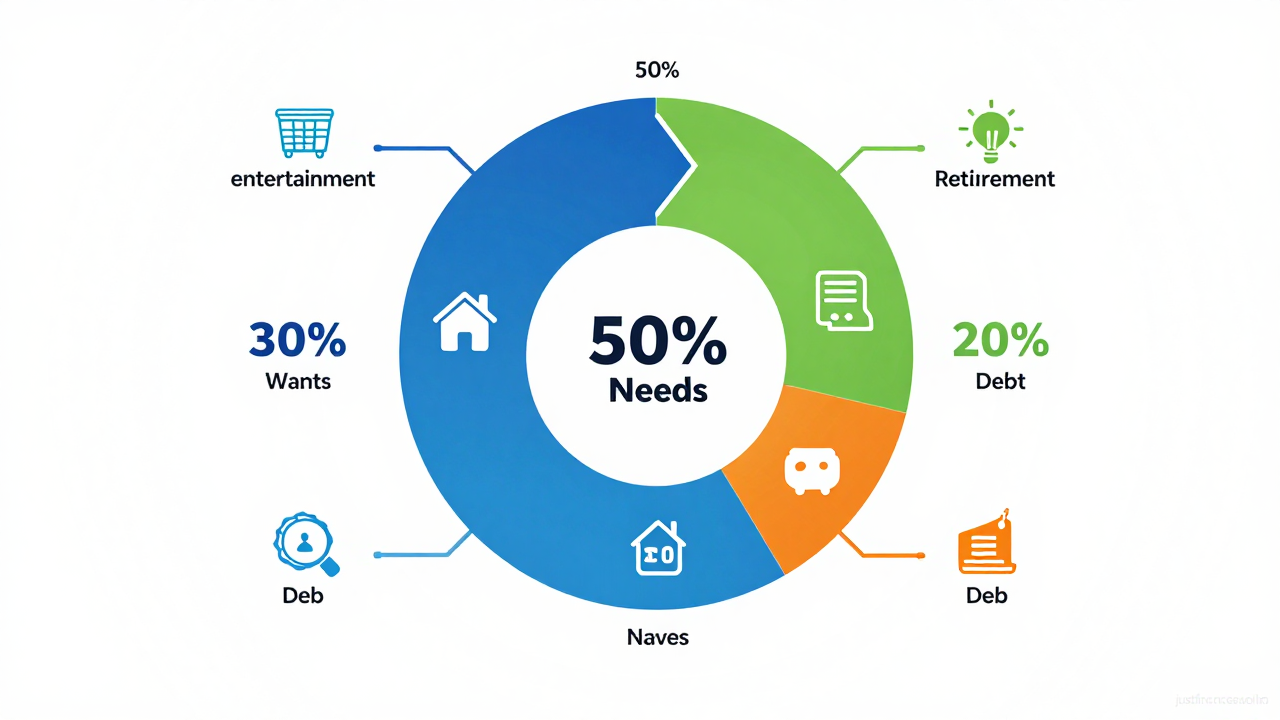

The 50/30/20 Rule for Everyday Balance

Category definitions: needs, wants, and savings

50 percent goes to needs. These are essential monthly commitments like rent or mortgage, utilities, groceries, and basic transportation. This is Budget Rules for Prosperity.

30 percent Discretionary spending goes to things you want. This is the enjoyable, non essential portion that improves quality of life, such as dining out, streaming, and hobbies.

20 percent goes to savings and debt payoff. This money builds your future through savings and accelerates debt repayment.

Practical examples and variations by income

Example A: Low income. Keep essentials tight. You might see needs take 60 percent, adjust wants downward, and still save a portion each month.

Example B: Middle income. Use the full 50/30/20 split. Maintain a balance between enjoying today and building tomorrow.

Example C: Higher income. You can boost savings or retirement contributions while still allowing for some wants. If debt is low, shift more to savings.

| Category | What it covers in your annual budget. | Example |

|---|---|---|

| Needs | Rent, utilities, groceries, transport | 600 on rent, 200 on utilities |

| Wants | Dining out, entertainment, upgrades | 150 for a movie plan |

| Savings & Debt | Savings account, retirement, debt payoff | 200 toward retirement |

Fidelity’s Plan Your Pay Framework

60% essential expenses, 30% nice-to-haves, 10% near-term goals and emergency savings

This framework helps you pace spending by dividing take-home pay into clear blocks. The aim is to cover basics, allow small pleasures, and build a safety net for tomorrow.

- 60% essential expenses cover housing costs, utilities, groceries, and transportation.

- 30% nice-to-haves fund small joys like meals out, entertainment, and hobbies.

- 10% near-term goals and emergency savings create a cushion for surprises and upcoming purchases.

Saving for retirement: 15% of pre-tax income

Fidelity recommends aiming for retirement contributions at 15% of earnings before taxes, including any employer matches. Starting early boosts growth even with modest contributions today.

| Part | What it covers | Example focus |

|---|---|---|

| 60% | Essential expenses | Rent, utilities, groceries |

| 30% | Nice-to-haves | Dining out, movies, hobbies |

| 10% | Near-term goals & emergency | Emergency fund, small goals |

The 60/30/10+15 Budget Template

Split by take-home pay and retirement contributions

This plan uses your take-home pay to split money into clear parts. It also adds a steady retirement check to grow your future financial goals. It keeps life simple and steady.

- 60% essential expenses cover housing, bills, food, and transport.

- 30% lifestyle spending includes meals out, hobbies, and small treats.

- 10% near-term goals and savings build a cushion for surprises and big purchases.

- Aim for 15% retirement contributions in your annual budget. Make a budget to go toward a retirement account when you receive your paycheck.

Adapting the plan to life’s changes

Life changes like a new job, a move, or a family addition can shift needs and wants. Adjust the amounts with care.

- When income rises, increase savings and retirement first.

- If expenses go up, trim wants but keep essentials secure.

- Big events get a special fund set aside in the near-term savings bucket.

| Part | What it covers | Typical aim |

|---|---|---|

| 60% Essential | Rent, utilities, groceries, transport | Keep basics covered |

| 30% Lifestyle | Dining, entertainment, hobbies | Enjoy now, without overspending by managing your money wisely. |

| 10% Near-term & Savings | Emergency fund, short-term goals | Build security |

| 15% Retirement | Retirement contributions | Grow long-term wealth |

The 40-30-20-10 Rule for Wealth Builders

Allocations for needs, wants, savings, and debt reduction

This framework divides your income into four clear buckets, helping you build wealth without sacrificing today.This is Budget Rules for Prosperity

- 40% needs cover housing, utilities, groceries, and transportation.

- 30% wants fund enjoyable activities and lifestyle upgrades.

- 20% savings goes toward an emergency cushion, retirement, and future goals.

- 10% debt reduction accelerates payoff on credit cards and loans.

When to adjust percentages for goals

Life changes call for thoughtful tweaks. Start with small shifts to keep balance intact.

- If faster debt payoff is the aim, shift a bit from discretionary spending to debt reduction.

- If early retirement is the goal, gradually boost the savings share.

- If housing costs rise, shore up needs first and trim wants modestly.

| Category | What it covers | Typical aim |

|---|---|---|

| Needs | Rent or mortgage, utilities, groceries, transport | Keep essentials secure |

| Wants | Dining out, entertainment, hobbies | Enjoy life without overspending by sticking to your budget. |

| Savings | Emergency fund, retirement, goals | Build a strong financial cushion |

| Debt reduction | Loans, credit card payoff | Shrink debt over time |

The 70-20-10 Guideline for Stability and Growth

Living within means

This rule helps you spend wisely and stay steady. It asks you to allocate most of your money to needs while reserving a portion for what you enjoy.

- 70% needs cover rent or mortgage, utilities, groceries, and transport.

- 20% wants pay for things you enjoy, like meals out or hobbies.

- 10% savings goes toward future goals and safety nets.

Saving aggressively

Boosting savings early compounds your wealth. It creates a cushion for tough times and accelerates long-term plans.This is Budget Rules for Prosperity

- Increase the savings share when you get raises or find extra income.

- Maintain a steady pace so you can sustain it month to month.

- Track how savings are used to see real progress.

Investing strategically

Put a portion of saved money into growth vehicles. Think retirement accounts and other long-term plans.

- Choose simple options that fit your risk tolerance.

- Pair with automatic transfers to keep contributions consistent.

- Review investments periodically to stay aligned with your goals.

Tuning the rule for early retirement goals

If early retirement is the aim, nudge allocations toward savings and investments while keeping needs covered.

| Category | What it covers | Typical aim |

|---|---|---|

| 70% Needs | Rent, utilities, groceries, transport | Secure basics |

| 20% Wants | Dining, entertainment, relax | Enjoy now with care |

| 10% Savings | Emergency fund, retirement, goals | Build future wealth |

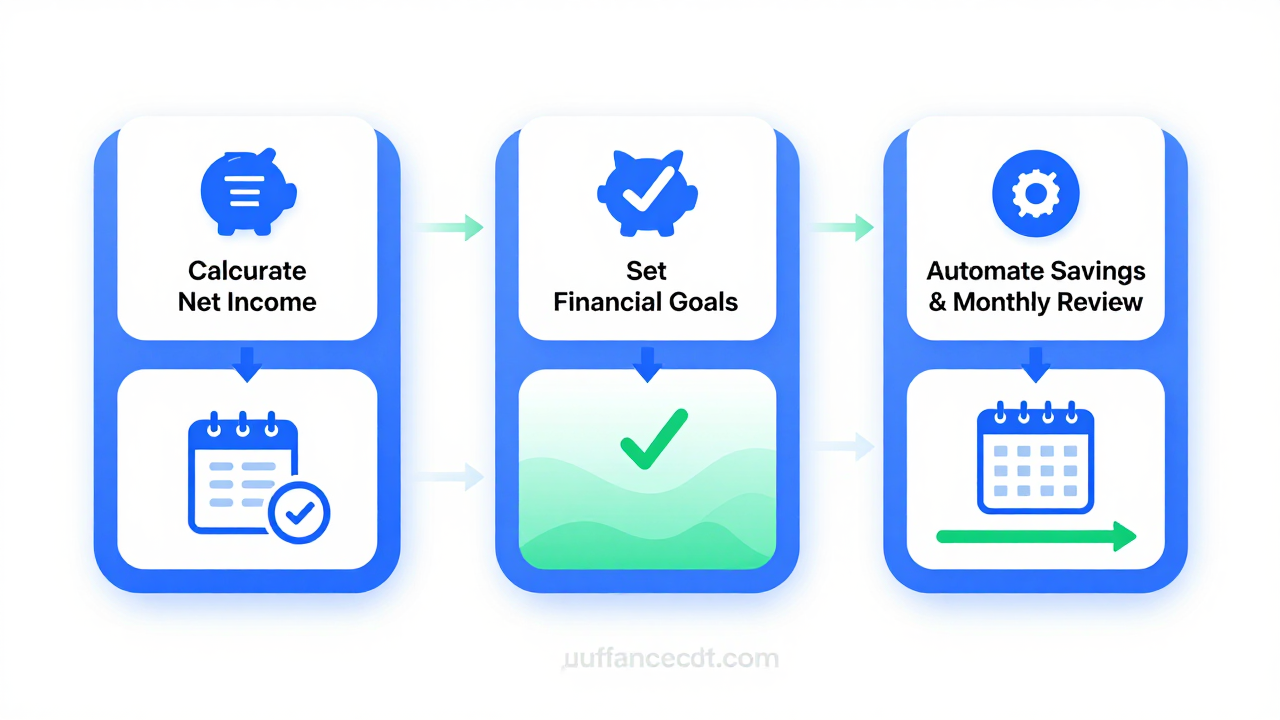

Step-by-Step Budget Construction

Calculate net income and track expenses

Know what you truly bring home. Net income is what you get after taxes and deductions. Track all spending to see where every dollar goes.This is Budget Rules for Prosperity

- Write down take-home pay from each paycheck.

- List every expense you pay each month.

- Identify fixed costs like rent or mortgage and variable costs like groceries.

Set realistic goals and build a plan

Small, clear goals keep you motivated. A solid plan shows where money goes each month and how you reach long-term aims.

- Choose 2-3 concrete goals, such as building an emergency fund or starting retirement savings.

- Allocate money into three or four simple categories you can manage.

- Write a simple budget plan you can review weekly.

Automate savings and review cadence

Automatic transfers make savings easy. A steady review keeps you on track and ready to adjust.

- Set automatic transfers to a savings account each payday.

- Review your budget once a month to catch changes early.

- Adjust allocations if your monthly income or expenses shift to stick to your budget.

| Step | What to do | Benefit |

|---|---|---|

| 1 | Calculate net income and track expenses | See true money flows |

| 2 | Set goals and build a plan | Clear path to progress |

| 3 | Automate savings and review cadence | Consistent growth |

Tools and Habits to Sustain Prosperity

Spending tracking tools

Track every dollar with a method that fits your routine. Choose a ledger, spreadsheet, or app you’ll actually use.

- Record daily purchases and categorize them quickly.

- Align every purchase with needs, wants, or savings to see real impact.

- Review your week to spot small leaks before they add up.

Envelope or digital budgeting methods

Give each dollar a clear purpose to stop mindless spending.

- Envelope method: allocate cash into three categories: needs, wants, and savings envelopes.

- Digital method: create virtual envelopes or separate accounts for each bucket.

- Keep a separate fund for irregular costs like gifts, repairs, or annual discounts.

Regular reviews, adjustments, and accountability

Consistency beats intensity. Build a cadence that keeps you on track.

- Set a fixed monthly review to reassess goals and allocations.

- Share progress with a trusted accountability partner who cheers you on.

- Celebrate small wins to keep motivation high and momentum steady.

FAQ

Got quick answers about budgeting rules. Here are clear responses to common questions.

- What is the 50-30-20 rule? It splits take-home pay into needs, wants, and savings. About half goes to needs, a third to wants, and one-fifth to savings and goals.

- What is a paycheck budget? It uses the money you actually bring home after taxes. Plan how to spend and save that amount each month.

- How can I start with 70-20-10? List your needs, set aside savings, and allocate 10 percent for debt or wealth building. Customize labels to fit your financial goals.

- What counts as needs? Essentials like rent or mortgage, utilities, groceries, and health care.

- What counts as wants? Extras you enjoy but can live without, such as streaming subscriptions or dining out.

- How do I automate savings to meet my financial goals? Set automatic transfers from your paycheck or checking to a savings or retirement account each payday.

- Why track spending? It reveals where money leaks happen and helps you stay in control of your finances.

- What is an emergency fund? A cash stash you can tap for unexpected bills, so you stay steady when surprises hit.

| Question | Short Answer |

|---|---|

| Which rule is easiest to start? | 50-30-20 for simple guidance, then tailor as needed. |

| How much should I save? | Start with a small goal, aim for at least 10% of take-home pay, then grow over time. |

If you want more help, you can tailor a budget plan that fits your life and keeps your money on track. You deserve financial calm today. 🎯

Conclusion

Key takeaways for adopting budget rules

Prosperity comes from a simple, repeatable plan. Choose a rule that fits your life and stay consistent. Keep essentials covered while you save for the future. Small, steady steps in managing your money beat big, chaotic shifts. Your money grows when you budget with purpose and move funds with intention.

- Choose a budgeting method that fits your routine.

- Automate savings to build your emergency fund and retirement.

- Review monthly to keep your finances balanced.

Next steps to begin your prosperity journey

- Calculate your monthly income after taxes and deductions.

- List needs and wants to set clear categories.

- Set up automatic transfers to a savings account and retirement accounts.

- Choose a rule like 50-30-20 or 70-20-10 and apply it to your paycheck budgeting.

| Action | What changes | Benefit |

|---|---|---|

| Choose rule | Aligns with goals | Clear path forward |

| Automate savings | Consistent growth | Less manual effort |

| Track monthly | Spot issues early | Stay on track |